The Longevity Wealth Trap

Picture this: it's 2041, and a 78-year-old man named Julian is sitting at his kitchen table, staring at a bank statement that shows a balance he never expected to see - zero. He did everything right. He saved diligently for 40 years, retired at 65 with what every calculator told him was more than enough, and lived modestly. The problem? He kept living. And living. And living.

This is the Longevity Wealth Trap - one of the most quietly devastating financial phenomena of our era. It doesn't announce itself with a market crash or a bad investment. It creeps in slowly, year by year, as the calendar pages turn and the account balance shrinks. The longer you live, the deeper the trap gets.

Why Living Longer Is a Financial Risk Nobody Talks About

- The retirement math was built for a shorter life

- Traditional retirement models were designed around a life expectancy of roughly 70-75 years. A 65-year-old retiree was expected to fund perhaps a decade of post-work life.

- Today, a healthy 65-year-old in the U.S. has a very real chance of living into their late 80s or even 90s - meaning they may need to fund 25 or 30 years of retirement, not 10.

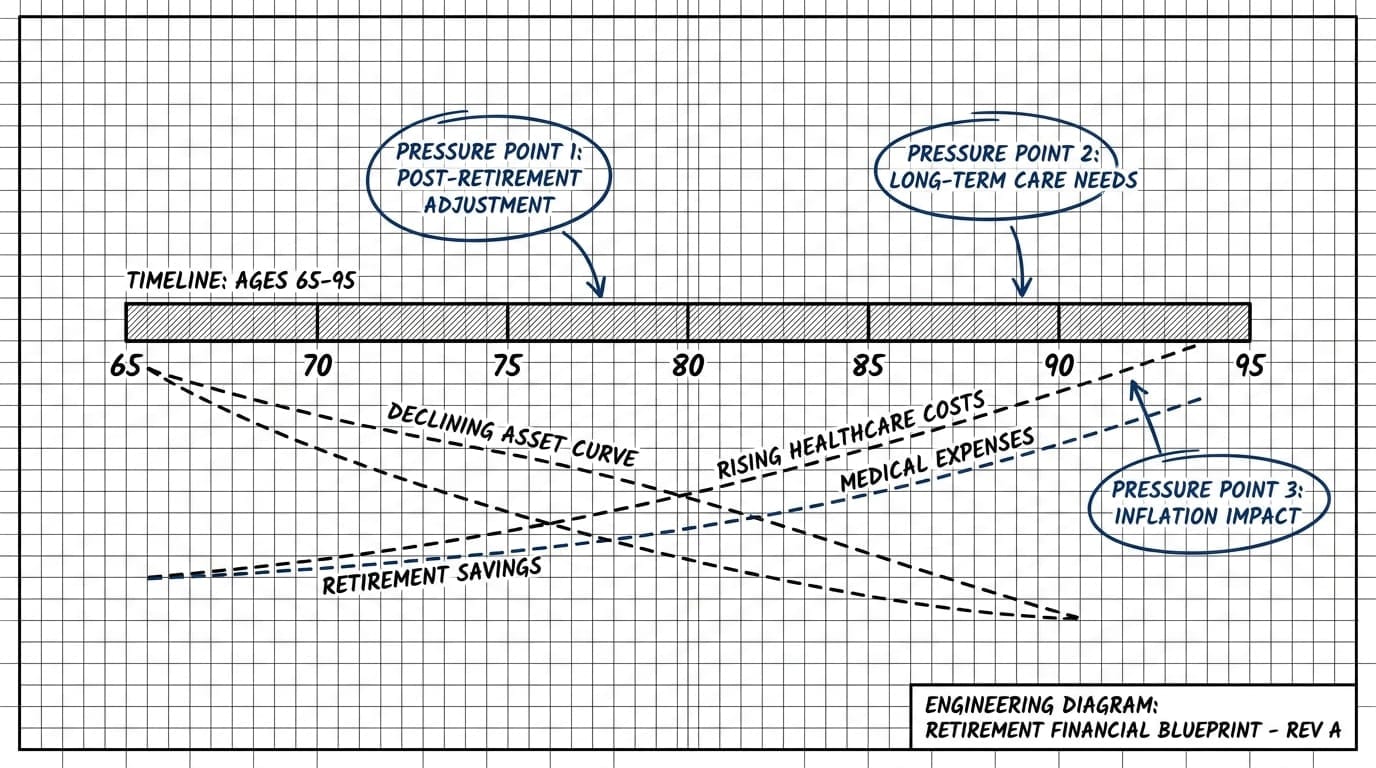

- The math simply doesn't hold. A nest egg calibrated for 12 years of withdrawals starts hemorrhaging value around year 18, leaving retirees financially exposed during their most medically vulnerable years.

- Inflation compounds the damage silently

- Even modest inflation at 3% per year cuts the purchasing power of a fixed income nearly in half over 25 years. What covers groceries and rent at 65 barely covers one of those things at 85.

- Healthcare costs - historically rising faster than general inflation - hit hardest precisely when retirees are oldest and most dependent on them.

- This double pressure of longer timelines plus eroding purchasing power is what turns a comfortable retirement into a financial emergency in slow motion.

- Social safety nets were never designed to carry the full load

- Social Security in the U.S. was conceived as a supplement to personal savings, not a primary income source. Yet for roughly 40% of older Americans, it represents the majority of their retirement income.

- Pension plans - once the backbone of retirement security - have been largely replaced by 401(k)s, shifting the entire burden of investment risk onto individuals who may lack the financial literacy to manage it.

- The result is a generation of retirees who are one bad market year away from a structural shortfall with no institutional safety net to catch them.

How to Reframe Your Wealth Strategy Around a Longer Life

- Plan for age 95, not age 80

- Financial planners increasingly recommend building retirement models around a 30-year horizon as a baseline. It feels excessive until it isn't.

- This means recalculating your safe withdrawal rate - the classic 4% rule starts to strain under a 30-year model, with many experts now suggesting 3% to 3.5% for longer-lived retirees.

- Running the numbers with a longer runway forces you to save more aggressively during your working years, which is uncomfortable but far less uncomfortable than running out of money at 82.

- Build income streams that don't expire

- Annuities, dividend-generating portfolios, and rental income all share one critical feature: they can generate cash flow regardless of how long you live, unlike a fixed lump sum that depletes over time.

- Delaying Social Security benefits to age 70 - rather than claiming at 62 or 65 - can increase monthly payments by as much as 76%, a powerful hedge against a very long retirement.

- The goal is to architect a financial life where your income is tied to time passing, not to a shrinking pool of capital.

- Account for the healthcare wildcard

- Fidelity estimates that the average 65-year-old couple will need roughly $315,000 in today's dollars just to cover healthcare costs in retirement - and that figure climbs every year.

- Long-term care insurance, Health Savings Accounts (HSAs), and dedicated healthcare reserves are not optional extras for long-lived retirees; they are structural necessities.

- Ignoring this line item in your retirement plan is like building a house without a roof - everything looks fine until the first storm hits.

The Longevity Wealth Trap is not a punishment for living well. It's a structural mismatch between how long modern humans actually live and how most financial systems were designed to support them. The good news? Awareness is the first move. Once you see the trap clearly - its mechanics, its timeline, its pressure points - you can start building a financial architecture that doesn't just survive a long life, but is genuinely built for one. The goal was never just to retire. The goal is to stay retired.